When a foreign company establishes a subsidiary in Japan, decisions made before incorporation can have a significant impact on ongoing tax costs. Several factors — including the amount of paid-in capital, the ratio of equity to debt, the fiscal year-end, and the design of intercompany transactions — are difficult or costly to change after submitting the first tax return.

This article organizes key tax issues that foreign companies should confirm and decide before establishing a Japan subsidiary. A summary checklist is included at the end.

Note: For the tax filings and procedures required after incorporation (such as the corporate establishment notification and the blue return application), please refer to our separate article, “Post-Incorporation Tax Checklist for Japan Subsidiaries.” (English article coming soon)

- Step 1: Branch or Subsidiary?

- Step 2: KK (Kabushiki Kaisha) or GK (Godo Kaisha)?

- Setting Paid-In Capital: One Number, Multiple Tax Impacts

- Capital Structure: Equity vs. Shareholder Loans

- Related-Party Transactions

- Pre-Incorporation Tax Checklist

- Conclusion

Step 1: Branch or Subsidiary?

The first question to address when entering the Japanese market is whether to operate through a branch of the foreign corporation or to establish a Japan subsidiary (a separate legal entity). The two structures are treated very differently for Japanese tax purposes.

In broad terms, a branch should be subject to Japanese corporate income tax only on its Japan-source income, while a subsidiary — as a domestic corporation — should be subject to corporate income tax on its worldwide income. A branch may offer the ability to offset start-up losses against the foreign parent’s income in certain jurisdictions, but it generally carries higher administrative complexity and greater tax audit risk in Japan.

→ For details, see: Setting Up in Japan: Branch vs. Subsidiary — A Tax Comparison

The remainder of this article assumes that a subsidiary is being established.

Step 2: KK (Kabushiki Kaisha) or GK (Godo Kaisha)?

Once the decision to establish a subsidiary has been made, the next question is whether to form a Kabushiki Kaisha (KK, company limited) or a Godo Kaisha (GK, limited liability company).

A KK has greater name recognition and credibility in Japan but involves higher incorporation costs and ongoing governance requirements — shareholders’ meetings, director term renewals, and public financial disclosure. A GK has lower incorporation costs (registration tax is approximately half that of a KK), no requirement for notarization of articles of incorporation or public financial disclosure, and a simpler decision-making structure. It is worth noting that many well-known foreign companies, including major technology firms, operate their Japan entities as GKs.

From a tax perspective, there is virtually no difference between a KK and a GK. The choice is primarily a legal, cost, and governance decision.

Setting Paid-In Capital: One Number, Multiple Tax Impacts

Paid-in capital is often treated as a purely financial decision, but in Japan it simultaneously affects multiple taxes. Importantly, the thresholds are not aligned — each tax uses a different breakpoint, and minimizing tax cost under one rule may push the company over a threshold in another. Modeling the full picture before incorporation is essential.

A note on terminology: Japanese tax law uses both “paid-in capital” (the stated capital registered with the legal authorities) and “total paid-in capital and capital surplus” (stated capital plus capital surplus). At incorporation, up to half of the amount paid in may be credited to capital surplus rather than stated capital. Several of the thresholds below refer to stated capital alone; others use the combined total. This distinction is noted in each section.

Corporate Tax — SME Preferential Rates

Companies with paid-in capital of JPY 100 million or less should generally be eligible for the SME preferential corporate tax rate of 15% on the first JPY 8 million of annual taxable income, compared with the standard rate of 23.2%.

However, foreign-owned subsidiaries should pay particular attention: even if the Japan subsidiary’s own paid-in capital is JPY 100 million or less, it should not qualify as an SME — and the preferential rate should not apply — if the subsidiary is wholly owned by a company with paid-in capital of JPY 500 million or more. This exclusion effectively covers most subsidiaries of large foreign corporations.

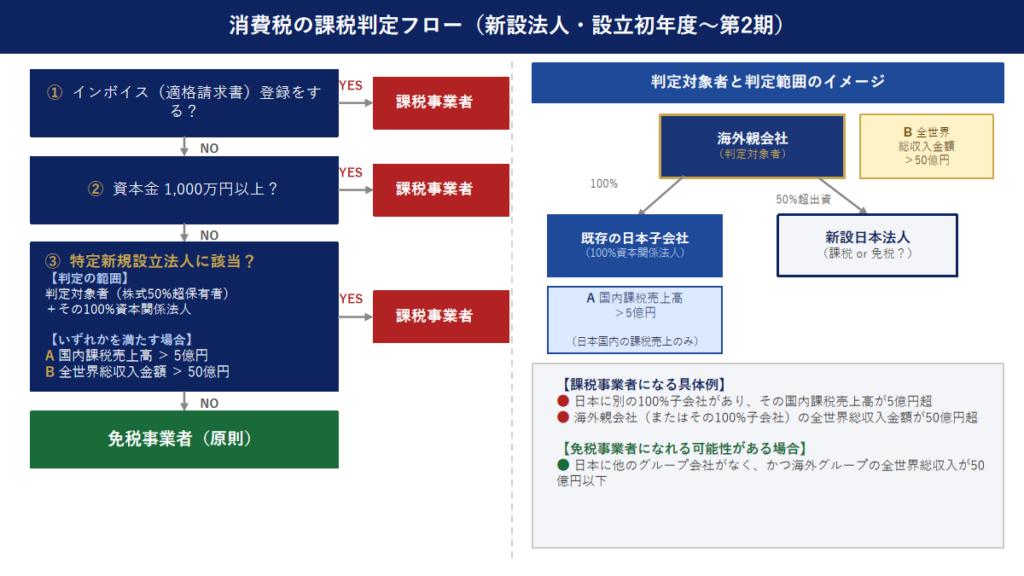

Japanese Consumption Tax (JCT) — Tax-Exempt Status

A newly established company may be able to avoid JCT obligations for its first two fiscal years, subject to three considerations.

① Invoice registration

If the subsidiary operates in a B-to-B environment where customers require qualified invoices (under Japan’s invoice system, introduced in October 2023), registering as a qualified invoice issuer is effectively mandatory for conducting business. Such registration requires JCT taxable status from the outset, making the exemptions below irrelevant. Confirm this point first before analyzing the other two.

② Paid-in capital threshold

For companies that do not register for the invoice system, JCT status for the first two fiscal years should depend on paid-in capital:

- Paid-in capital below JPY 10 million: in principle, the company should be treated as a tax-exempt entity in Years 1 and 2.

- Paid-in capital of JPY 10 million or more: the company should be treated as a JCT taxable entity from its first fiscal year.

③ Group-wide revenue test

Even where paid-in capital is below JPY 10 million, the group-wide revenue test may cause the subsidiary to be treated as a taxable entity. These rules are designed to prevent large corporate groups from using small new entities to obtain a JCT exemption.

The rules should apply where a person or entity directly or indirectly holding more than 50% of the new subsidiary’s shares (a “controlling person”) — or any entity in which the controlling person holds 100% of the shares — meets either of the following:

- Japan-source taxable sales subject to JCT exceeding JPY 500 million in the relevant prior period

- Worldwide total revenue exceeding JPY 5 billion (applicable to fiscal years beginning on or after October 1, 2024)

Practical considerations

To illustrate when these rules are likely to apply in practice:

- Where the foreign parent already holds another Japan subsidiary as a 100% owned entity, and that subsidiary’s Japan-source taxable sales exceed JPY 500 million in the relevant period, the group-wide revenue test should apply to the newly established company.

- Where the foreign parent (or any entity in which the foreign parent holds 100% of the shares) has worldwide total revenue exceeding JPY 5 billion, the rules should similarly apply.

Conversely, where the group has no other companies in Japan and the foreign parent’s worldwide total revenue does not exceed JPY 5 billion, a newly established subsidiary with paid-in capital below JPY 10 million may be able to qualify as a tax-exempt entity for JCT purposes. Confirming the group structure and the revenue figures of each group entity before incorporation is therefore important.

Note: The above explanation of JCT obligations is simplified. In practice, there are additional rules that may affect taxable status — including mandatory taxation upon acquisition of certain high-value assets, and the effect of filing a consumption tax taxable entity election form. These are not covered in this article.

Inhabitants’ Tax — Per Capita Levy and Income-Based Levy

Inhabitants’ tax — local tax imposed by prefectures and municipalities — has two components.

The per capita levy is a fixed annual charge that applies regardless of whether the company is profitable. In Tokyo’s 23 special wards, the combined per capita levy ranges from JPY 70,000 per year (for companies with paid-in capital of JPY 10 million or less and 50 or fewer employees) up to JPY 1.21 million or more for larger companies. This is an unavoidable fixed cost from the first fiscal year.

The income-based levy is calculated as a percentage of the corporate tax liability. A surtax rate should apply where paid-in capital exceeds JPY 100 million, or where the corporate tax liability for the year exceeds JPY 10 million. In Tokyo, the surtax rate is 10.4% (compared with the standard rate of 7.0%).

Enterprise Tax — Size-Based Enterprise Tax

For companies with paid-in capital exceeding JPY 100 million, enterprise tax should be calculated on a size basis. In addition to the income base (taxable income), two further components are levied:

- Value added base: broadly, personnel costs, net interest expense, and net rent, adjusted for the net profit or loss. Rate: 1.26% (Tokyo).

- Capital base: the total paid-in capital and capital surplus. Rate: 0.525% (Tokyo).

Because the value added base and capital base apply regardless of profitability, a company subject to size-based enterprise tax may face an enterprise tax liability even in a loss-making year. Companies with paid-in capital of JPY 100 million or less should be subject to enterprise tax on the income base only (up to 7.48% in Tokyo, for companies above certain annual income or revenue thresholds).

2024 Tax Reform — Extended Scope of Size-Based Enterprise Tax

An important change effective for fiscal years beginning on or after April 1, 2026 significantly expands the scope of size-based enterprise tax. Under this change, size-based enterprise tax should apply even if the Japan subsidiary’s own paid-in capital is JPY 100 million or less, provided all of the following conditions are met:

- The company is a 100% subsidiary (directly or indirectly) of a corporation whose total paid-in capital and capital surplus exceeds JPY 5 billion (a “specified large corporation”)

- The subsidiary’s own paid-in capital at fiscal year-end is JPY 100 million or less

- The subsidiary’s total paid-in capital and capital surplus at fiscal year-end exceeds JPY 200 million

For subsidiaries of foreign parents that meet the JPY 5 billion threshold, keeping the Japan subsidiary’s total paid-in capital and capital surplus at JPY 200 million or below should be required to remain outside the scope of size-based enterprise tax. A transitional relief measure reduces the additional tax burden by two-thirds for fiscal years beginning between April 1, 2026 and March 31, 2027, and by one-third for fiscal years beginning between April 1, 2027 and March 31, 2028.

Summary: Paid-In Capital Thresholds and Their Tax Impacts

| Tax | Assessment basis | Key threshold | Key impact |

|---|---|---|---|

| Corporate tax | Paid-in capital | JPY 100 million | ≤ JPY 100M: SME preferential rate (15%) on first JPY 8M of taxable income may apply. Note: Not available if the subsidiary is wholly owned by a company with paid-in capital ≥ JPY 500M — which covers most large foreign groups. > JPY 100M: Standard rate (23.2%) applies. |

| Japanese consumption tax (JCT) | Paid-in capital | JPY 10 million | < JPY 10M: In principle, tax-exempt in Years 1–2. ≥ JPY 10M: Taxable from Year 1. Exemption may be unavailable regardless of paid-in capital where: (i) invoice registration is required, or (ii) the group-wide revenue test applies. |

| Inhabitants’ tax (per capita levy) | Paid-in capital and capital surplus (combined) | Multiple: JPY 10M / 100M / 1B / 5B | Fixed annual charge regardless of profit. Tokyo 23 wards (≤ 50 employees): ranges from JPY 70,000 to JPY 1.21M+ per year. An unavoidable fixed cost from the first fiscal year. |

| Inhabitants’ tax (income-based levy) | Paid-in capital | JPY 100M (or corporate tax ≥ JPY 10M) | ≤ JPY 100M and corporate tax < JPY 10M: Standard rate (7.0%, Tokyo). > JPY 100M, or corporate tax ≥ JPY 10M: Surtax rate (10.4%, Tokyo) applies. |

| Enterprise tax | Paid-in capital | JPY 100 million | ≤ JPY 100M: Income base only (up to 7.48%, Tokyo). Higher marginal rate; no size-based components. > JPY 100M: Size-based enterprise tax applies. Value added base (1.26%) and capital base (0.525%) are levied in addition to income base (1.18%) — even in a loss-making year. |

| Enterprise tax (2024 reform — FY beginning on/after 1 April 2026) | Total paid-in capital and capital surplus | JPY 200M (if parent’s total ≥ JPY 5B) | Where the parent’s total paid-in capital and capital surplus exceeds JPY 5 billion, size-based enterprise tax should apply to the Japan subsidiary if its own total paid-in capital and capital surplus exceeds JPY 200 million. To avoid this, the subsidiary’s combined paid-in capital and capital surplus should be kept at JPY 200 million or below. |

Where invoice registration is required (as is practically the case for most B-to-B businesses), the JCT exemption is unavailable, and the primary objective becomes minimizing the tax burden across the remaining taxes. In that scenario, setting paid-in capital at JPY 100 million or less and keeping total paid-in capital and capital surplus at JPY 200 million or below should allow the company to benefit from SME treatment for corporate tax, the standard inhabitants’ tax rate, and income-base-only enterprise tax.

The above is a simplified overview. The optimal paid-in capital level will depend on the specific business, financial projections, and group structure. Since paid-in capital is difficult to change after incorporation, consulting with a tax adviser before setting this figure is strongly recommended.

Capital Structure: Equity vs. Shareholder Loans

Why It Matters

When funding a Japan subsidiary, the foreign parent may choose between contributing equity (paid-in capital and capital surplus) or extending a shareholder loan. Dividend payments on equity are not deductible for Japanese corporate tax purposes, while interest payments on shareholder loans are generally deductible. This creates an incentive to fund the subsidiary primarily with debt, which reduces its taxable income in Japan.

However, Japanese tax law contains two sets of rules specifically designed to limit excessive debt funding by foreign-owned subsidiaries. Both should be analyzed as part of the capital structure design before incorporation.

Thin Capitalization Rules

Under Japan’s thin capitalization rules, where the total borrowings from foreign controlling shareholders exceed three times the company’s equity, the interest on the excess borrowings should be non-deductible for corporate tax purposes.

For example: a subsidiary with equity of JPY 10 million and a shareholder loan of JPY 40 million has borrowings of JPY 10 million in excess of the three-times threshold (3 × JPY 10 million = JPY 30 million). The interest corresponding to that excess should not be deductible.

A structure designed to minimize paid-in capital while maximizing shareholder loans carries the risk that the thin capitalization rules eliminate the intended tax benefit. Running the numbers before finalizing the capital structure is essential.

→ For details, see: “Thin Capitalization and Earnings Stripping Rules in Japan” (English article coming soon)

Earnings Stripping Rules

In addition to the thin capitalization rules, Japan’s earnings stripping rules provide that where net interest expense exceeds 20% of adjusted taxable income (broadly equivalent to EBITDA), the excess net interest should be non-deductible.

Unlike the thin capitalization rules, the earnings stripping rules apply to interest paid not only to foreign controlling shareholders but also to third-party lenders. Disallowed interest amounts may generally be carried forward for up to seven years (with special provisions for certain fiscal years).

Where the subsidiary carries significant debt from any source, both rules should be modeled together.

→ For details, see: “Thin Capitalization and Earnings Stripping Rules in Japan” (English article coming soon)

Related-Party Transactions

Transfer Pricing

Under Japan’s transfer pricing rules, transactions between the Japan subsidiary and related foreign entities (“foreign affiliated transactions”) must be priced at arm’s length — that is, as if conducted between independent parties. Where the pricing departs from this standard, the tax authorities may adjust the subsidiary’s taxable income.

Key issues to address before incorporation include:

- Types of intercompany transactions that will arise — royalties, management fees, goods sales, intra-group services, loans, etc.

- The transfer pricing methodology to be applied to each transaction type (e.g., comparable uncontrolled price, cost-plus, resale price, etc.)

- Whether contemporaneous documentation will be required: mandatory where total foreign affiliated transactions for the fiscal year exceed JPY 5 billion, or where intangible asset transactions exceed JPY 300 million

If intercompany transactions begin from the first fiscal year, commencing operations without a clear pricing policy and supporting documentation creates a risk of transfer pricing adjustments in a subsequent tax audit. Preparing contracts and pricing documentation before the subsidiary commences operations is advisable.

→ For details, see: “Transfer Pricing in Japan: Fundamentals, Documentation, and Practical Issues” (English article coming soon)

Withholding Tax (WHT) and Tax Treaty Filing

Payments from the Japan subsidiary to the foreign parent — such as royalties, interest, and dividends — should generally be subject to Japanese withholding tax at the domestic rate of 20.42%. Where an applicable tax treaty provides for a reduced or zero rate, that benefit should be available provided a Tax Treaty Application Form is filed with the relevant tax office no later than the day before the payment date.

For subsidiaries that expect to make payments to the parent from an early stage, mapping out the treaty filing schedule before incorporation is important.

→ For details, see: “Japan Withholding Tax and Tax Treaty Series” (English articles coming soon)

Pre-Incorporation Tax Checklist

| Category | Key issues to confirm before incorporation | Related article (EN) |

|---|---|---|

| Entity structure (1) | Branch or subsidiary? | Branch vs. Subsidiary |

| Entity structure (2) | KK or GK? | — |

| Paid-in capital (corporate tax) | Check whether parent’s paid-in capital is JPY 500 million or more. SME preferential rates are typically unavailable for subsidiaries of large foreign groups regardless of the Japan subsidiary’s own paid-in capital. | — |

| Paid-in capital (JCT) | ① Confirm whether invoice registration is required (B-to-B businesses: typically yes). ② If no invoice registration: assess JPY 10M paid-in capital threshold. ③ Assess group-wide revenue test: confirm Japan-source taxable sales and worldwide total revenue of the controlling group. | — |

| Paid-in capital (inhabitants’ tax) | Simulate per capita levy at each threshold (JPY 10M / 100M / 1B / 5B). Confirm whether income-based levy surtax rate will apply. | — |

| Paid-in capital (enterprise tax) | Confirm size-based enterprise tax applicability (JPY 100M paid-in capital threshold). If parent’s total paid-in capital and capital surplus ≥ JPY 5B: confirm whether JPY 200M combined threshold will be breached (2024 reform). Model initial years including expected loss periods. | — |

| Capital structure | Determine equity vs. shareholder loan ratio. Run thin capitalization simulations (3× equity threshold). Run earnings stripping simulations (20% of adjusted taxable income threshold). | Coming soon |

| Related-party transactions | Identify types of intercompany transactions (royalties, management fees, goods, services, etc.). Determine transfer pricing methodology for each transaction. Assess documentation requirements (mandatory if foreign affiliated transactions ≥ JPY 5B or intangible transactions ≥ JPY 300M). | Coming soon |

| Withholding tax / tax treaties | Identify applicable tax treaty and reduced WHT rates. Map out Tax Treaty Application Form filing schedule — must be submitted before the first payment date. | Coming soon |

| Foreign Exchange and Foreign Trade Act | Confirm whether the business falls within a designated industry (financial services, telecommunications, defence-related, etc.) requiring a pre-registration notification to the Ministry of Finance. Filing may be required before the incorporation registration. | — |

Note on Foreign Exchange and Foreign Trade Act: Certain industries (e.g., financial services, telecommunications, defence-related) are designated under the Foreign Exchange and Foreign Trade Act, and a pre-registration notification to the Ministry of Finance and/or relevant ministries may be required before the incorporation registration. Confirm whether the business falls within a designated industry at an early stage.

Conclusion

When establishing a Japan subsidiary, it is easy to focus on the registration and procedural aspects and overlook the underlying tax design decisions. As this article has shown, paid-in capital alone affects corporate tax, JCT, inhabitants’ tax, and enterprise tax simultaneously — and often in conflicting directions. Capital structure and intercompany transaction design add further complexity with immediate practical consequences.

The following points deserve particular attention:

- Paid-in capital affects multiple taxes at different thresholds; the right level depends on the group structure, business model, and financial projections.

- The thin capitalization rules and earnings stripping rules engage from day one; the capital structure should be stress-tested before incorporation.

- Transfer pricing and withholding tax issues arise from the first intercompany transaction — not just at the time of a tax audit.

These issues are unlikely to be visible in the company registration paperwork, and many foreign companies encounter them only at the time of their first Japanese tax filing — by which point options may be limited.

For the tax filings and procedures required after incorporation, please refer to our separate article, “Post-Incorporation Tax Checklist for Japan Subsidiaries.” (English article coming soon)

The tax rules described in this article are simplified for explanatory purposes. When actually establishing a Japan subsidiary, we recommend consulting with a tax adviser experienced in international and Japanese corporate tax at an early stage.

コメント